Readers of Tabbush Report www.tabbushreport.comwill know of our long-standing positive view on US banks, driven by multiple facets. Our presentation to clients last year is just as relevant today, which can be summarized as Banks: Ultimate Leverage. With the JPM results and some other, less followed banks, the story for US banks, continues to look strong, and still in the early stages. We remind, that a view on smaller, more niche banks, can be incredibly rewarding, and also where patterns, themes can be more visible, sooner, than with large, mainstream banks.

JPM reports a strong rise in net interest income during the quarter, which will be one of the key changes that most are looking for. This is core. This is not credit costs. Even where net interest margins are not yet rising, the absolute increase of net interest income can mark the beginning of positive change, unlike what banks had seen since early last year. As and when loan:deposit ratios (LDR) rise, with a re-pricing of fixed deposits downward, and with accelerating loan volume, the delta here can be even more substantial.

One of the smallest banks in the US is Third Century Bancorp (TDCB). It shows how this can occur, even in the face of incredibly low and rapidly falling interest rates, all during last year, and through 3Q21. Loan mix will also have an impact. With TDCB, it becomes clearer, outside the traditional money center banks and even large regionals, how net interest income can swell - it is not only bank analysis theory.

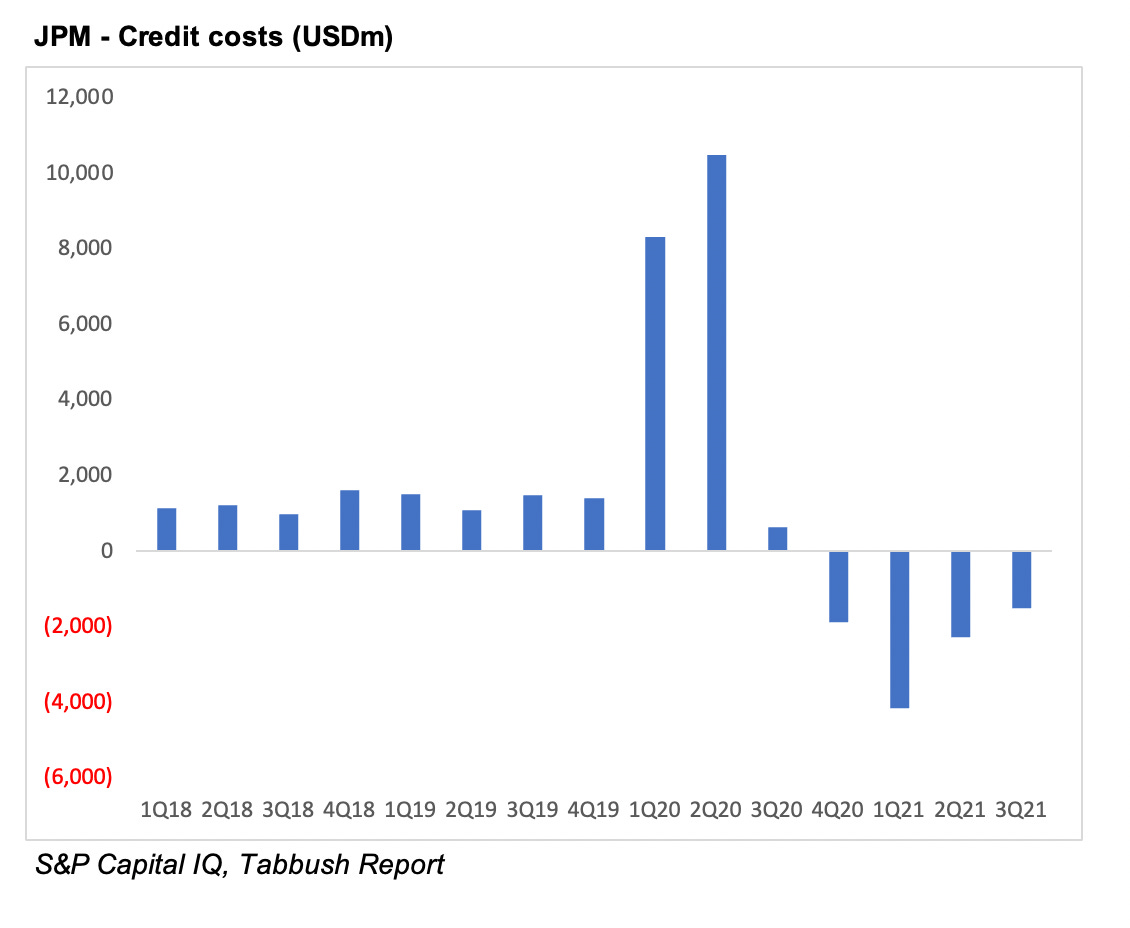

The theme of improving credit metrics and reversals or benign credit costs, continues. Generally, these major themes are not limited to 3 or 6 months, and especially when considering the current calamity for banks, and the incredibly high provisioning done in a very short span of time, during early FY20. We have seen in the US, high-frequency data for lending growth, and the delta in consumer lending growth has been especially strong. It is no wonder that JPM has seen a sizable positive delta with its credit card net-charge offs, which is a key driver to the bank’s benign credit costs.

While recent credit cost volume compared with normal credit cost volume, is certainly one way to consider normalization and quarterly credit cost estimates we can also look to total loan loss reserve (LLR) build. As and when banks take write-backs these will come from LLR, leaving less cushion to absorb loan losses. Where LLR remains higher, there is technically, more of a pool from which to draw reversals.

JPM now reports LLR at USD18.2bn which is down from USD28.3bn at the peak. And this is where its reversals have come from. Its LLR though remains nearly 40% higher than in FY19. A look across US and global banks, focussing on where LLR is today compared with FY19 can provide a strong signal for credit costs in coming quarters. However, this is not the sole factor that will drive credit costs - there are many that must be considered. For US banks and many in Asia, we see a multitude of positive drivers for bank profit, where credit costs is just one item, and which does not appear to be exhausted.

For our institutional product, speak to us on info@tabbushreport.com to discuss offering and pricing.